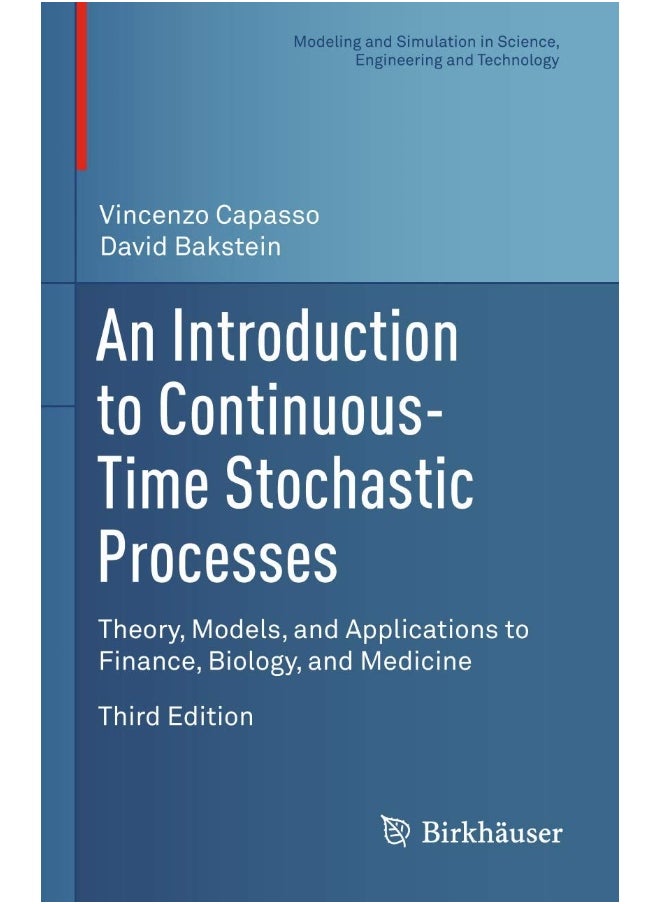

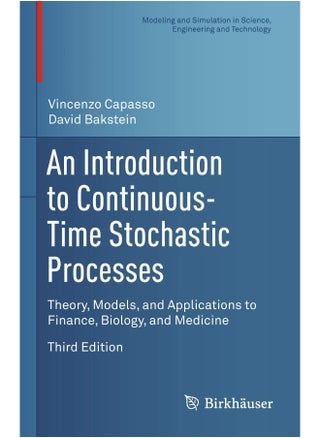

| وصف الكتاب | This textbook, now in its third edition, offers a rigorous and self-contained introduction to the theory of continuous-time stochastic processes, stochastic integrals, and stochastic differential equations. Expertly balancing theory and applications, the work features concrete examples of modeling real-world problems from biology, medicine, industrial applications, finance, and insurance using stochastic methods. No previous knowledge of stochastic processes is required. Key topics include: Markov processes Stochastic differential equations Arbitrage-free markets and financial derivatives Insurance risk Population dynamics, and epidemics Agent-based models New to the Third Edition: Infinitely divisible distributions Random measures Levy processes Fractional Brownian motion Ergodic theory Karhunen-Loeve expansion Additional applications Additional exercises Smoluchowski approximation of Langevin systems An Introduction to Continuous-Time Stochastic Processes, Third Edition will be of interest to a broad audience of students, pure and applied mathematicians, and researchers and practitioners in mathematical finance, biomathematics, biotechnology, and engineering. Suitable as a textbook for graduate or undergraduate courses, as well as European Masters courses (according to the two-year-long second cycle of the “Bologna Scheme”), the work may also be used for self-study or as a reference. Prerequisites include knowledge of calculus and some analysis; exposure to probability would be helpful but not required since the necessary fundamentals of measure and integration are provided. From reviews of previous editions: "The book is ... an account of fundamental concepts as they appear in relevant modern applications and literature. ... The book addresses three main groups: first, mathematicians working in a different field; second, other scientists and professionals from a business or academic background; third, graduate or advanced undergraduate students of a quantitative subject related to stochastic theory and/or applications." -Zentralblatt MATH |

استرجاع مجاني وسهل

استرجاع مجاني وسهل أفضل العروض

أفضل العروض

![/fashion-men/jack_jones/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-04.png)

![/fashion-men/seventy_five/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-01.png)

![/fashion-men/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-02.png)

![/fashion-women/mango/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-05.png)

![/fashion-women/guess/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-09.png)

![/fashion-women/ella/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-01.png)

![/fashion-women/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-02.png)

![/fashion/view-all-kids-clothing/nike/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-01.png)

![/fashion/view-all-kids-clothing/disney/disney_minnie_mouse/disney_frozen/disney_princess/disney_mickey_mouse/disney_baby/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-03.png)

![/fashion/view-all-kids-clothing/new_balance/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-11.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/chloris/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-04.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/roland/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-05.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/donner/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-06.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/korg/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-07.png)