English

- استرجاع مجاني وسهل

- أفضل العروض

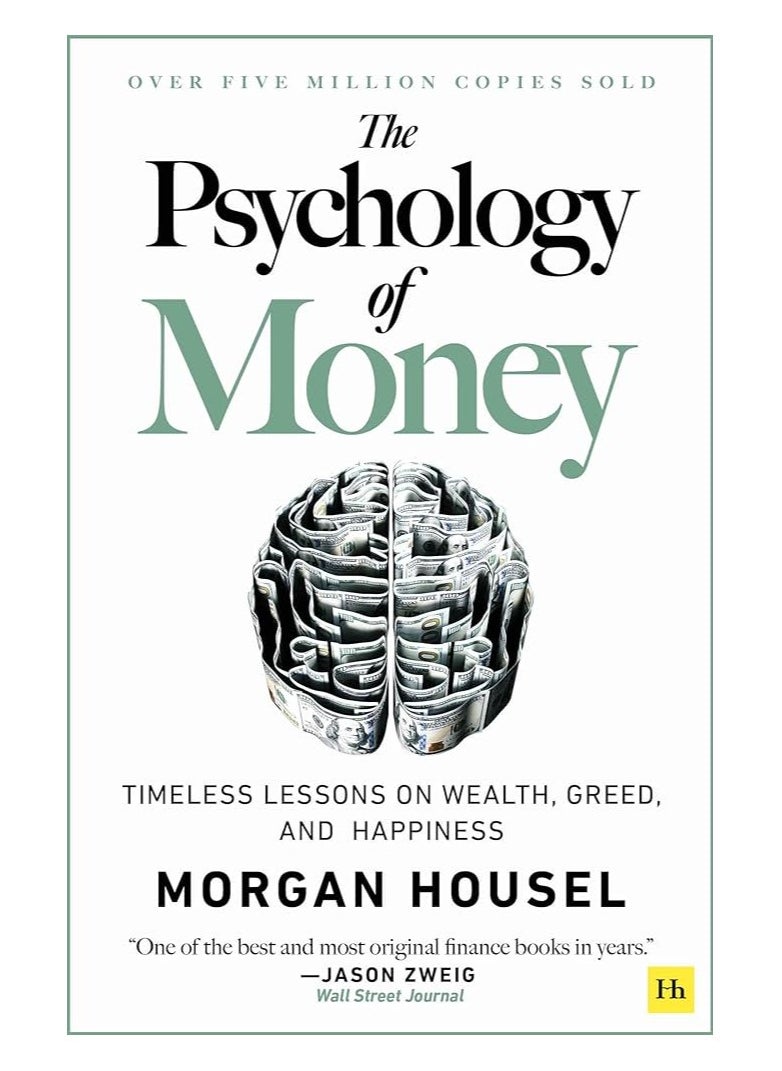

Commodities And Commodity Derivatives Hardcover English by Helyette Geman - 25-Mar-05

الآن:

750.00 د.إ.شامل ضريبة القيمة المضافة

توصيل مجاني

توصيل مجاني باقي 1 وحدات في المخزونتوصيل مجانيباقي 1 وحدات في المخزون

باقي 1 وحدات في المخزونتوصيل مجانيباقي 1 وحدات في المخزون

احصل عليه غدًا

احصل على د.إ. 37.50 رصيد مسترجع باستخدام بطاقة بنك المشرق نون الائتمانية. اشترك الآن. قدّم الحين

ادفع على 4 دفعات بدون فوائد بقيمة ١٨٧٫٥٠ د.إ.اعرف المزيد

قسمها على 4 دفعات ب ١٨٧٫٥٠ د.إ. بدون فوائد أو رسوم تأخير.اعرف المزيد

1

توصيل مجاني لنقطة نون ومراكز الاستلام

معرفة المزيد

إرجاع سهل لكل المنتجات في هذا العرض.

المنتج كما في الوصف

70%

شريك لنون منذ

4+ سنينالمواصفات

| الناشر | John Wiley and Sons Ltd |

| رقم الكتاب المعياري الدولي 13 | 9780470012185 |

| اللغة | الإنجليزية |

| العنوان الفرعي للكتاب | Modeling And Pricing For Agriculturals, Metals And Energy |

| وصف الكتاب | The last few years have been a watershed for the commodities, cash and derivatives industry. New regulations and products have led to an explosion in the commodities markets, creating a new asset for investors that includes hedge funds as well as University endowments, and has resulted in a spectacular growth in spot and derivative trading. This book covers hard and soft commodities (energy, agriculture and metals) and analyses: * Economic and geopolitical issues in commodities markets * Commodity price and volume risk * Stochastic modelling of commodity spot prices and forward curves * Real options valuation and hedging of physical assets in the energy industry It is required reading for energy companies and utilities practitioners, commodity cash and derivatives traders in investment banks, the Agrifood business, Commodity Trading Advisors (CTAs) and Hedge Funds. In Commodities and Commodity Derivatives, Helyette Geman shows her powerful command of the subject by combining a rigorous development of its mathematical modelling with a compact institutional presentation of the arcane characteristics of commodities that makes the complex analysis of commodities derivative securities accessible to both the academic and practitioner who wants a deep foundation and a breadth of different market applications. It is destined to be a "must have" on the subject." --Robert Merton, Professor, Harvard Business School "A marvelously comprehensive book of interest to academics and practitioners alike, by one of the worlda s foremost experts in the field." --Oldrich Vasicek, founder, KMV |

| المراجعة التحريرية | ...expect to see this book become the bible of the field... (Short Book Review, June 2006) |

| عن المؤلف | Helyette Geman is a Professor of Finance at the University Paris Dauphine and ESSEC Graduate Business School. She is a graduate of the Ecole Normale Superieure in mathematics, holds a Masters degree in theoretical physics and a PhD in mathematics from the University Pierre et Marie Curie and a PhD in Finance from the University Pantheon Sorbonne. Professor Geman has been a scientific advisor to a number of major energy companies for the last decade, covering the spectrum of oil, natural gas and electricity as well as agricultural commodities origination and trading. She was previously the head of Research and Development at Caisse des Depots. She has published more than 40 papers in major finance journals including the Journal of Finance, Mathematical Finance, Journal of Financial Economics, Journal of Banking and Finance and Journal of Business. She has also written a book entitled Insurance and Weather Derivatives'. Professor Geman's research includes asset price modelling using jump--diffusions and Levy processes, commodity forward curve modelling and exotic option pricing for which she won the first prize of the Merrill Lynch Awards. |

| تاريخ النشر | 25-Mar-05 |

| عدد الصفحات | 416 |

Commodities And Commodity Derivatives Hardcover English by Helyette Geman - 25-Mar-05

تمت الإضافة لعربة التسوق

مجموع السلة 750.00 د.إ.