English

- استرجاع مجاني وسهل

- أفضل العروض

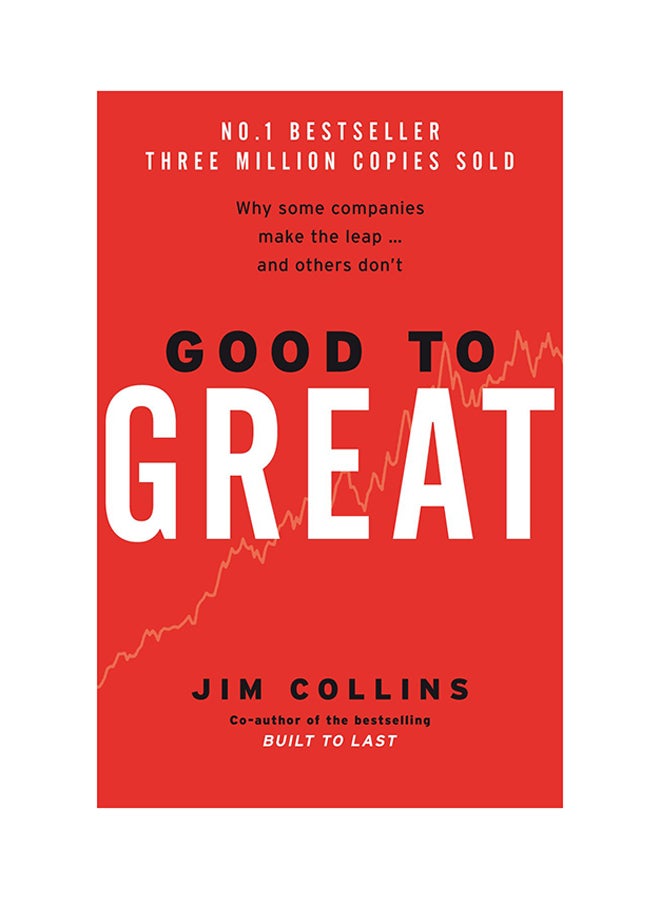

Financial Risk Management : Applications In Market, Credit, Asset And Liability Management And Firmwide Risk hardcover english - 12 October 2015

الآن:

454.85 د.إ.شامل ضريبة القيمة المضافة

توصيل مجاني

توصيل مجاني باقي 1 وحدات في المخزونتوصيل مجانيباقي 1 وحدات في المخزون

باقي 1 وحدات في المخزونتوصيل مجانيباقي 1 وحدات في المخزون

احصل عليه غدًا

احصل على د.إ. 22.74 رصيد مسترجع باستخدام بطاقة بنك المشرق نون الائتمانية. اشترك الآن. قدّم الحين

ادفع على 4 دفعات بدون فوائد بقيمة ١١٣٫٧١ د.إ.اعرف المزيد

قسمها على 4 دفعات ب ١١٣٫٧١ د.إ. بدون فوائد أو رسوم تأخير.اعرف المزيد

1

توصيل مجاني لنقطة نون ومراكز الاستلام

معرفة المزيد

إرجاع سهل لكل المنتجات في هذا العرض.

المنتج كما في الوصف

80%

شريك لنون منذ

7+ سنينالمواصفات

| الناشر | John Wiley & Sons Inc |

| رقم الكتاب المعياري الدولي 13 | 9781119135517 |

| اللغة | الإنجليزية |

| العنوان الفرعي للكتاب | Applications In Market, Credit, Asset And Liability Management And Firmwide Risk |

| وصف الكتاب | Transform your approach to oprisk modelling with a proven, non-statistical methodologyOperational Risk Modeling in Financial Services provides risk professionals with a forward-looking approach to risk modelling, based on structured management judgement over obsolete statistical methods. Proven over a decade's use in significant banks and financial services firms in Europe and the US, the Exposure, Occurrence, Impact (XOI) method of operational risk modelling played an instrumental role in reshaping their oprisk modelling approaches; in this book, the expert team that developed this methodology offers practical, in-depth guidance on XOI use and applications for a variety of major risks.The Basel Committee has dismissed statistical approaches to risk modelling, leaving regulators and practitioners searching for the next generation of oprisk quantification. The XOI method is ideally suited to fulfil this need, as a calculated, coordinated, consistent approach designed to bridge the gap between risk quantification and risk management. This book details the XOI framework and provides essential guidance for practitioners looking to change the oprisk modelling paradigm.Survey the range of current practices in operational risk analysis and modellingTrack recent regulatory trends including capital modelling, stress testing and moreUnderstand the XOI oprisk modelling method, and transition away from statistical approachesApply XOI to major operational risks, such as disasters, fraud, conduct, legal and cyber riskThe financial services industry is in dire need of a new standard -- a proven, transformational approach to operational risk that eliminates or mitigates the common issues with traditional approaches. Operational Risk Modeling in Financial Services provides practical, real-world guidance toward a more reliable methodology, shifting the conversation toward the future with a new kind of oprisk modelling. |

| عن المؤلف | Jimmy Skoglund is principal product manager of global risk products at SAS. He has more than fifteen years of market experience developing and implementing risk methodologies, and his articles have appeared in such publications as the Journal of Risk, Journal of Banking and Finance, and Journal of Risk Management in Financial Institutions. Jimmy holds a PhD from the Stockholm School of Economics. Wei Chen is director of stress testing solutions at SAS. He has more than fifteen years' experience in risk analytics and technology in banking and insurance, and he is an associate editor of the Journal of Risk Model Validation. His publications have appeared in several journals including Journal of Risk and Journal of Risk Model Validation. Wei holds a PhD from the University of Iowa. |

| تاريخ النشر | 12 October 2015 |

| عدد الصفحات | 576 |

Financial Risk Management : Applications In Market, Credit, Asset And Liability Management And Firmwide Risk hardcover english - 12 October 2015

تمت الإضافة لعربة التسوق

مجموع السلة 454.85 د.إ.