English

- استرجاع مجاني وسهل

- أفضل العروض

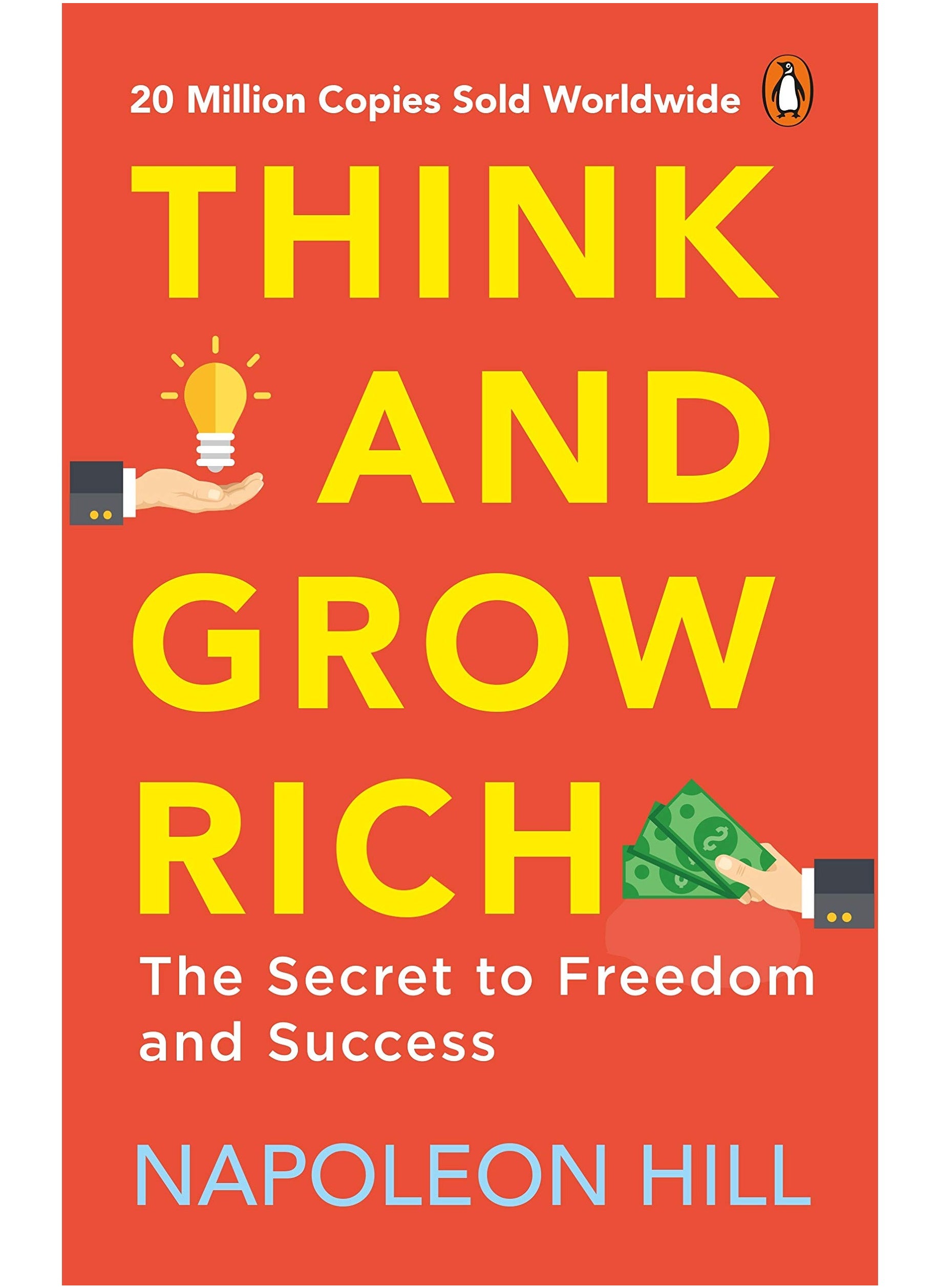

How To Calculate Options Prices And Their Greeks : Exploring The Black Scholes Model From Delta To Vega Hardcover English by Pierino Ursone - 2 June 2015

الآن:

د.إ. 318.00 شامل ضريبة القيمة المضافة

توصيل مجاني

توصيل مجاني

احصل عليه خلال 19 - 22 مارس

احصل على د.إ. 15.90 رصيد مسترجع باستخدام بطاقة بنك المشرق نون الائتمانية. اشترك الآن. قدّم الحين

1

توصيل مجاني لنقطة نون ومراكز الاستلام

معرفة المزيد

إرجاع سهل لكل المنتجات في هذا العرض.

المواصفات

| الناشر | John Wiley & Sons Inc |

| رقم الكتاب المعياري الدولي 13 | 9781119011620 |

| رقم الكتاب المعياري الدولي 10 | 1119011620 |

| تنسيق الكتاب | غلاف صلب |

| اللغة | الإنجليزية |

| العنوان الفرعي للكتاب | Exploring The Black Scholes Model From Delta To Vega |

| وصف الكتاب | A unique, in-depth guide to options pricing and valuing their greeks, along with a four dimensional approach towards the impact of changing market circumstances on options How to Calculate Options Prices and Their Greeks is the only book of its kind, showing you how to value options and the greeks according to the Black Scholes model but also how to do this without consulting a model. You'll build a solid understanding of options and hedging strategies as you explore the concepts of probability, volatility, and put call parity, then move into more advanced topics in combination with a four-dimensional approach of the change of the P&L of an option portfolio in relation to strike, underlying, volatility, and time to maturity. This informative guide fully explains the distribution of first and second order Greeks along the whole range wherein an option has optionality, and delves into trading strategies, including spreads, straddles, strangles, butterflies, kurtosis, vega-convexity , and more. Charts and tables illustrate how specific positions in a Greek evolve in relation to its parameters, and digital ancillaries allow you to see 3D representations using your own parameters and volumes. The Black and Scholes model is the most widely used option model, appreciated for its simplicity and ability to generate a fair value for options pricing in all kinds of markets. This book shows you the ins and outs of the model, giving you the practical understanding you need for setting up and managing an option strategy. Understand the Greeks, and how they make or break a strategy See how the Greeks change with time, volatility, and underlying Explore various trading strategies Implement options positions, and more Representations of option payoffs are too often based on a simple two-dimensional approach consisting of P&L versus underlying at expiry. This is misleading, as the Greeks can make a world of difference over the lifetime of a strategy. How to Calculate Options Prices and Their Greeks is a comprehensive, in-depth guide to a thorough and more effective understanding of options, their Greeks, and (hedging) option strategies. |

| عن المؤلف | PIERINO URSONE has extensive option trading experience. He began his career as a Market Maker with Optiver, an international market maker that trades on all of the world's major financial markets. Afterwards, Ursone ran his own option trading company on the Dutch options exchange in Amsterdam, and after nine years in equity options, he entered the Energy commodity market, trading options on a proprietary basis. |

| تاريخ النشر | 2 June 2015 |

| عدد الصفحات | 224 |

How To Calculate Options Prices And Their Greeks : Exploring The Black Scholes Model From Delta To Vega Hardcover English by Pierino Ursone - 2 June 2015

تمت الإضافة لعربة التسوق

مجموع السلة 318.00 د.إ.