English

- استرجاع مجاني وسهل

- أفضل العروض

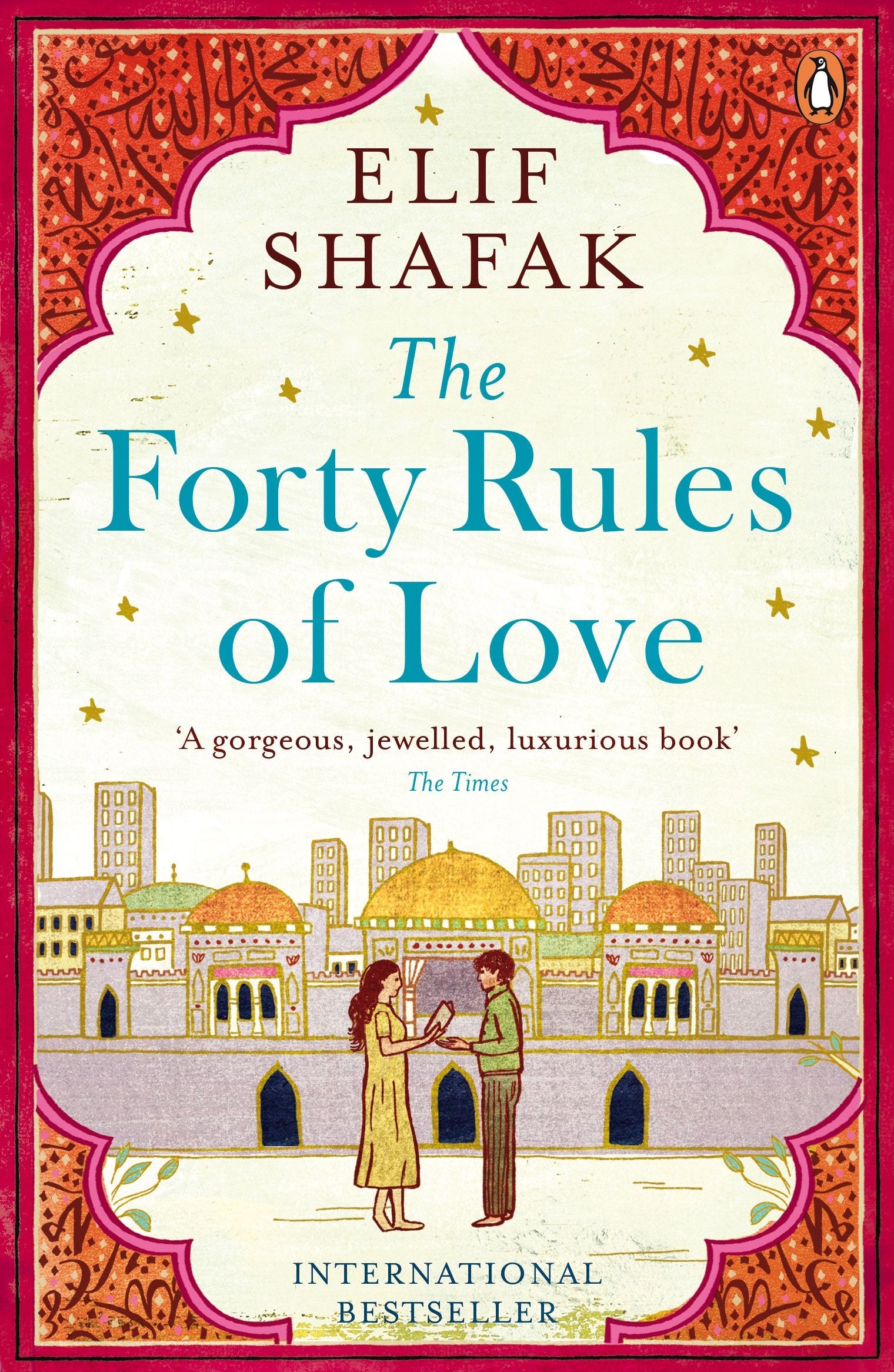

Quantitative Risk and Portfolio Management

قبل:

د.إ. 323.00

الآن:

د.إ. 314.00 شامل ضريبة القيمة المضافة

وفرّت:

د.إ. 9.00 د.إ.

توصيل مجاني

توصيل مجاني باقي 4 وحدات في المخزونتوصيل مجانيباقي 4 وحدات في المخزون

باقي 4 وحدات في المخزونتوصيل مجانيباقي 4 وحدات في المخزون

احصل عليه خلال 25 - 28 مارس

احصل على د.إ. 15.70 رصيد مسترجع باستخدام بطاقة بنك المشرق نون الائتمانية. اشترك الآن. قدّم الحين

1

توصيل مجاني لنقطة نون ومراكز الاستلام

معرفة المزيد

إرجاع سهل لكل المنتجات في هذا العرض.

المواصفات

| الناشر | Cambridge University Press |

| رقم الكتاب المعياري الدولي 13 | 9781009209045 |

| الكاتب | Kenneth J. Winston |

| تنسيق الكتاب | Hardcover |

| اللغة | English |

| وصف الكتاب | A comprehensive modern introduction to risk and portfolio management for quantitatively adept advanced undergraduate and beginning graduate students who will become practitioners in the field of quantitative finance. With a focus on real-world application, but providing a background in academic theory, this text builds a firm foundation of rigorous but practical knowledge. Extensive live data and Python code are provided as online supplements, allowing a thorough understanding of how to manage risk and portfolios in practice. With its detailed examination of how mathematical techniques are applied to finance, this is the ideal textbook for giving students with a background in engineering, mathematics or physics a route into the field of quantitative finance. |

| عن المؤلف | Kenneth J. Winston is a Lecturer in Economics at the California Institute of Technology and an Adjunct Professor of Mathematics at New York University. Having trained as a combinatorist at MIT, he moved into the field of quantitative finance, creating algorithms for equity and option investment strategies. He worked as a Chief Risk Officer at Western Asset Management and Morgan Stanley, and is a founder of the Buy Side Risk Managers Forum. Winston won the 2006 Roger Murray Award at the Institute for Quantitative Research in Finance and is a co-editor of The Oxford Handbook of Quantitative Asset Management (OUP: 2014). |

| تاريخ النشر | 20230921 |

| عدد الصفحات | 927 |

Quantitative Risk and Portfolio Management

تمت الإضافة لعربة التسوق

مجموع السلة 314.00 د.إ.