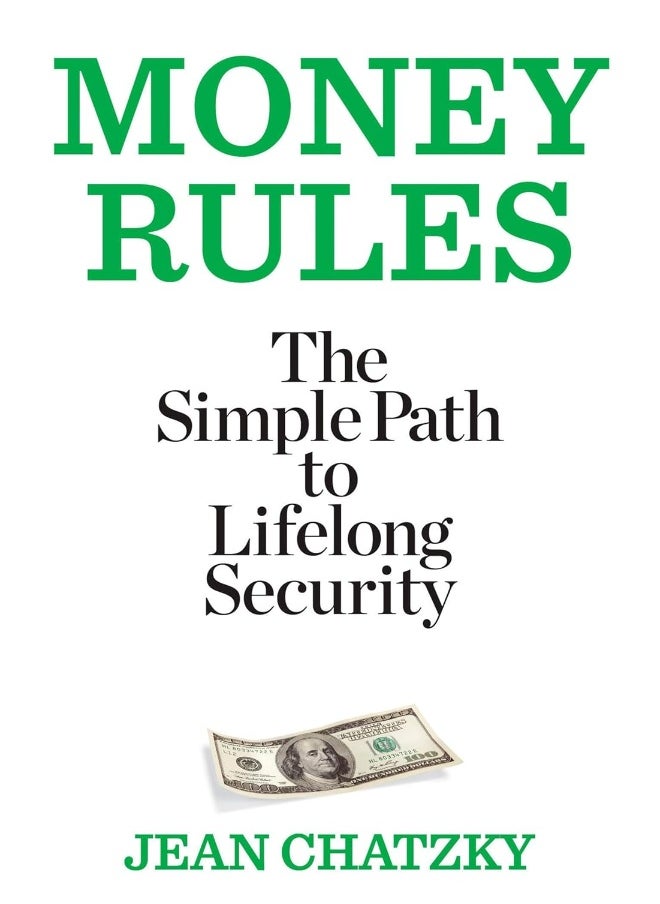

| About the Author | Jean Chatzky is the financial editor for NBC's Today and a columnist for Prevention. She is the author of five books, including the bestsellers Pay It Down and Make Money, Not Excuses. She lives in Westchester, NY. Excerpt. © Reprinted by permission. All rights reserved. PART 1Make MoneyThe money that goes out--whether you spend it, save it, invest it, or give it away--has to come from somewhere.That generally means earning it.And that's a good thing.Getting paid is an indication that others value what you do, how you think, and who you are.All of those things are a boost to your self-esteem.The rules in this section will help you understand how to earn what you're worth, how to extract the most happiness possible from those earnings, and when, in fact, you shouldn't do that particular work but instead delegate it to someone else.1. Your job is your most important investment.For years, you were told your home and retirement accounts were your greatest assets. Wrong. If the Great Recession has proven anything, it's that your job--more specifically, your earning power--is by far your greatest asset. Protect your financial security by treating this asset like any other investment. If your work profile is risky, you're paid on commission or bonuses rather than straight salary, or your job security is largely tied to the economy, it's like a stock. If it's more stable, you work for the government, you're one of the lucky few who still has a traditional pension plan, or you're a tenured teacher or college professor-- you're essentially holding a bond. Consider this when you fashion your asset allocation: Those in "stock-like" jobs need to account for that by being a little less aggressive in their other investments. Those with job security can take a little more risk.2. Your education is your second-most important investment.The rising cost of college has led to a populist cry that college degrees aren't worth the money. That's completely backward. A study from Georgetown University shows the value of a college degree is going up. The typical worker with less than a high school diploma will earn $973,000 over the course of a career. The typical professional (think doctor or lawyer) will earn $3.6 million. College grads fall halfway between. The pay gap between those who go to college and don't has gotten wider--and is expected to continue to grow. This isn't just an income gap--it's also a "social" one. College grads are more likely to get and stay married, to have strong networks of friends, to be active in their communities, and are less likely to be obese and smoke (both are wealth reducers--see rules . |

Free & Easy Returns

Free & Easy Returns Best Deals

Best Deals

![/fashion-men/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-01.png)

![/fashion-men/reebok/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-02.png)

![/fashion-men/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-03.png)

![/fashion-men/jack_jones/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-04.png)

![/fashion-men/american_eagle/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-05.png)

![/fashion-men/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-06.png)

![/fashion-men/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-07.png)

![/fashion-men/seventy_five/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-01.png)

![/fashion-men/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-02.png)

![/fashion-women/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-01.png)

![/fashion-women/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-03.png)

![/fashion-women/mango/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-05.png)

![/fashion-women/guess/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-09.png)

![/fashion-women/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-07.png)

![/fashion-women/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-06.png)

![/fashion-women/ella/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-01.png)

![/fashion-women/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-02.png)

![/fashion-women/american_eagle/?sort[by]=popularity&sort[dir]=desc&limit=50](https://f.nooncdn.com/cms/pages/20250317/womens/en_dk-nav-brands-09.png)

![/fashion/view-all-kids-clothing/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-02.png)

![/fashion/view-all-kids-clothing/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-04.png)

![/fashion/view-all-kids-clothing/nike/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-01.png)

![/fashion/view-all-kids-clothing/disney/disney_minnie_mouse/disney_frozen/disney_princess/disney_mickey_mouse/disney_baby/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-03.png)

![/fashion/view-all-kids-clothing/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-07.png)

![/fashion/view-all-kids-clothing/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-08.png)

![/fashion/view-all-kids-clothing/mothercare/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-06.png)

![/fashion/view-all-kids-clothing/kappa/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-10.png)

![/fashion/view-all-kids-clothing/new_balance/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-11.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/chloris/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-04.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/roland/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-05.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/donner/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-06.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/korg/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-07.png)