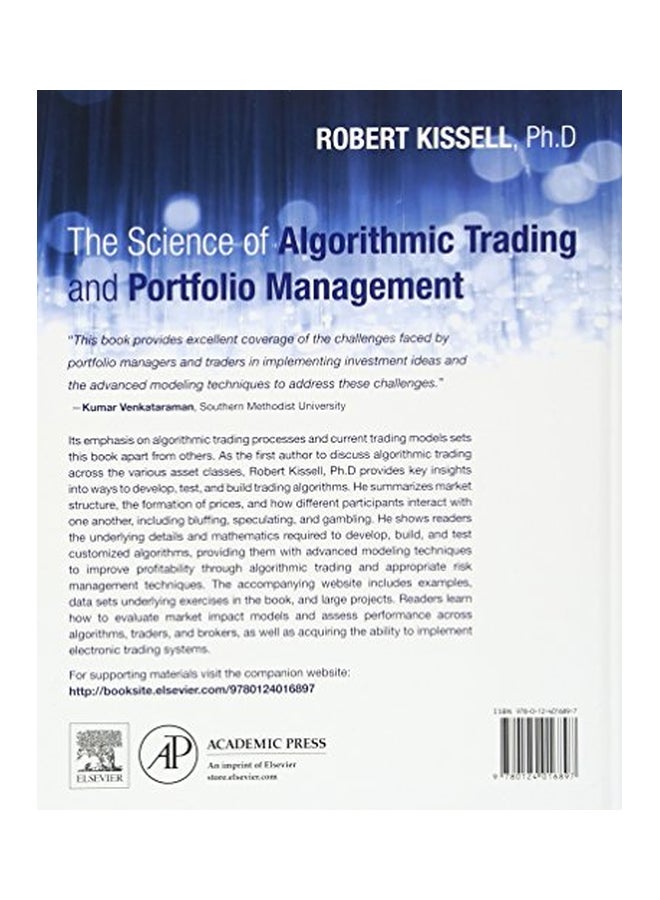

| About the Author | Dr. Robert Kissell is the president and founder of Kissell Research Group. He has over twenty years of experience specializing in economics, finance, math & statistics, risk, and sports modeling. Dr. Kissell is author of the leading industry books, "The Science of Algorithmic Trading & Portfolio Management," (Elsevier, 2013), "Multi-Asset Risk Modeling" (Elsevier, 2014), and "Optimal Trading Strategies," (AMACOM, 2003). He has published numerous research papers on trading, electronic algorithms, risk management, and best execution. His paper, "Dynamic Pre-Trade Models: Beyond the Black Box," (2011) won Institutional Investor's prestigious paper of the year award. Dr. Kissell is an adjunct faculty member of the Gabelli School of Business at Fordham University and is an associate editor of the Journal of Trading and the Journal of Index Investing. He has previously been an instructor at Cornell University in their graduate Financial Engineering program. Dr. Kissell has worked with numerous Investment Banks throughout his career including UBS Securities where he was Executive Director of Execution Strategies and Portfolio Analysis, and at JPMorgan where he was Executive Director and Head of Quantitative Trading Strategies. He was previously at Citigroup/Smith Barney where he was Vice President of Quantitative Research, and at Instinet where he was Director of Trading Research. He began his career as an Economic Consultant at R.J. Rudden Associates specializing in energy, pricing, risk, and optimization. During his college years, Dr. Kissell was a member of the Stony Brook Soccer Team and was Co-Captain in his Junior and Senior years. It was during this time as a student athlete where he began applying math and statistics to sports modeling problems. Many of the techniques discussed in "Optimal Sports Math, Statistics, and Fantasy" were developed during his time at Stony Brook, and advanced thereafter. Thus, making this book the byproduct of decades of successful research. Dr. Kissell has a Ph.D. in Economics from Fordham University, an MS in Applied Mathematics from Hofstra University, an MS in Business Management from Stony Brook University, and a BS in Applied Mathematics & Statistics from Stony Brook University. show less |

Free & Easy Returns

Free & Easy Returns Best Deals

Best Deals

![/fashion-men/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-01.png)

![/fashion-men/reebok/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-02.png)

![/fashion-men/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-03.png)

![/fashion-men/jack_jones/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-04.png)

![/fashion-men/american_eagle/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-05.png)

![/fashion-men/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-06.png)

![/fashion-men/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-men-brands-07.png)

![/fashion-men/seventy_five/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-01.png)

![/fashion-men/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-womens-new-brands-02.png)

![/fashion-women/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-01.png)

![/fashion-women/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-03.png)

![/fashion-women/mango/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-05.png)

![/fashion-women/guess/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-09.png)

![/fashion-women/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-07.png)

![/fashion-women/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240305/4ef48af441e2b44cea1673cd2e4aff67/en_dk-women-brands-06.png)

![/fashion-women/ella/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-01.png)

![/fashion-women/skechers/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20241812/en_dk-nav-brands-02.png)

![/fashion-women/american_eagle/?sort[by]=popularity&sort[dir]=desc&limit=50](https://f.nooncdn.com/cms/pages/20250317/womens/en_dk-nav-brands-09.png)

![/fashion/view-all-kids-clothing/adidas/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-02.png)

![/fashion/view-all-kids-clothing/puma/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-04.png)

![/fashion/view-all-kids-clothing/nike/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-01.png)

![/fashion/view-all-kids-clothing/disney/disney_minnie_mouse/disney_frozen/disney_princess/disney_mickey_mouse/disney_baby/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-03.png)

![/fashion/view-all-kids-clothing/tommy_hilfiger/tommy_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-07.png)

![/fashion/view-all-kids-clothing/calvin_klein/calvin_klein_jeans/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-08.png)

![/fashion/view-all-kids-clothing/mothercare/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-06.png)

![/fashion/view-all-kids-clothing/kappa/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-10.png)

![/fashion/view-all-kids-clothing/new_balance/?sort[by]=popularity&sort[dir]=desc&limit=50](https://a.nooncdn.com/cms/pages/20240911/nav-web/en_mb_uae_brand-11.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/chloris/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-04.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/roland/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-05.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/donner/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-06.png)

![/music-movies-and-tv-shows/musical-instruments-24670/pianos-keyboards-synthesizers/korg/?sort[by]=popularity&sort[dir]=desc&limit=50&page=1&isCarouselView=false](https://f.nooncdn.com/cms/pages/20250407/books-nav/en_uae_dk-nav-brands-07.png)